import pandas as pd

import matplotlib.pyplot as plt

from datetime import datetime

from statsmodels.tsa.stattools import grangercausalitytests

import pandas_datareader.data as web

import requests

from io import StringIO

start_date_str = '1979-01-01'

start_date = datetime.strptime(start_date_str,'%Y-%m-%d')

end_date = datetime.today()The Diminishing Returns of Education on Quality of Life: An Empirical Analysis of Macroeconomic Decoupling

Investigating the Causal Links Between M2 Monetary Expansion, Tuition Inflation, and the Erosion of Professional Career Stability

macro

economics

education policy

labor market

monetary policy

mental health

Abstract

This analysis challenges the traditional association between extended formal education and improved quality of life (QoL) by examining the structural breakdown of professional labor returns. Utilizing longitudinal data from 1979 to 2025, the study identifies a significant decoupling of real wages from productivity growth and a staggering disparity between tuition inflation and median income. Through Granger Causality tests, the research validates that expansions in the M2 money supply serve as a primary predictor for rising educational costs, effectively devaluing the net financial return of degrees. Furthermore, the application of a “Career Sharpe Ratio” framework reveals that higher education no longer functions as career insurance; rather, increased credentials often lead to higher income volatility that offsets marginal gains. The findings suggest a shift in the role of tertiary education from a tool for knowledge acquisition to a mechanism for “elite inclusion,” a transition that correlates with rising underemployment and a documented decline in the mental health and job satisfaction of highly educated professionals.

The Evolving Impact of Education on Quality of Life in the Context of M0/1/2/Consumer Inflation and Socioeconomic Shifts

This thesis explores the relationship between the length of formal education and overall quality of life (QoL), considering the evolving economic landscape influenced by M0/1/2/Consumer inflation. It hypothesizes that while extended education initially correlated with improved QoL through higher income, better employment, stable marriages, and overall well-being, lately, the benefits of prolonged education have diminished in the face of increasing economic pressures, competitive stress, and societal shifts. The study uses a combination of economic theory, quantitative data analysis, and sociological perspectives to examine how the changing cost-benefit dynamics of education affect life satisfaction in modern times.

Chapter 1: Introduction

Background

Education and Quality of Life: Historically, education has been seen as a key driver of social mobility and improved quality of life. Extended years in education have been associated with higher income, better job prospects, stable marriages, and improved health outcomes. M2 Inflation and Economic Environment: Over the past few decades, the global economic environment has been influenced by central banks’ monetary policies, including significant increases in M2 money supply. This has led to inflationary pressures, impacting the cost of education, living standards, and overall socioeconomic structures.

1.2 Research Problem

The traditional view that more education equates to better QoL is being challenged by new economic realities. Increasing costs of education, diminishing returns on educational investment, and changing societal expectations have altered the landscape.

1.3 Hypothesis

Up to a certain period, increased years of education correlated positively with improvements in QoL. However, as M0/1/2/Consumer inflation increased, leading to rising educational costs and altered economic dynamics, the benefits of prolonged education have diminished, even potentially reversing in certain cases.

Chapter 2: Quality of Life (QoL) Improvement Traditionally Associated with Years in Education

Long Years in Education, Job Stability and Income Mobility:

Income and Job Stability: Traditionally, longer years in education have been associated with higher income and better job stability. Research consistently shows that individuals with more education tend to earn more over their lifetimes and are less likely to be unemployed. This connection has been a key driver for the push towards extended education in many societies. No longer True.

Social Status and Mobility: Extended education has also been linked with higher social status and greater social mobility. The credentials obtained through prolonged education often serve as markers of social class, allowing individuals to access higher social and professional circles. No longer True.

Reducing Compensation Given a Productivity Level:

- Wage Stagnation: In recent decades, there has been growing concern that despite increasing levels of education, wages have not kept pace with productivity gains. This wage stagnation, coupled with rising education costs, has led to a situation where the financial returns on education may no longer justify the investment, thus reducing the perceived value of long-term education in improving QoL (World Bank).

- Underemployment: Many graduates find themselves in jobs that do not require the level of education they have attained, leading to underemployment. This mismatch between education and job requirements can contribute to dissatisfaction and frustration.

High Competitive Stress:

Mental Health Impacts: As the demand for higher education has increased, so has the competition, leading to significant stress among students. The pressure to perform well academically to secure top-tier jobs has contributed to a rise in mental health issues, including anxiety and depression. This competitive stress can negate some of the QoL improvements associated with higher education (World Bank).

Work-Life Imbalance: The need to excel in education often leads to work-life imbalances, where students and young professionals may sacrifice leisure and family time for academic or career success, potentially reducing overall life satisfaction.

Sedentary Lifestyles of Educated Individuals:

Health Implications: Higher levels of education are often associated with sedentary jobs, such as office work, which can lead to health issues like obesity, cardiovascular diseases, and mental health problems. The sedentary lifestyle that accompanies many highly educated professions may undermine the health benefits that should accompany better employment and income (Our World in Data).

Reduced Physical Activity: As people spend more time in education and subsequently in knowledge-intensive jobs, they may have less time for physical activities, which negatively impacts their overall well-being. T-leves for men.

High-Demand from Partners Selection (Female):

Marital Satisfaction and Selection Pressure: Educated individuals, especially women, may face higher expectations in partner selection, leading to delays in marriage or dissatisfaction due to mismatched expectations. The emphasis on finding a partner with similar educational or socioeconomic status can create additional stress and reduce life satisfaction (Our World in Data).

Family Dynamics: Higher education levels can lead to different expectations in family roles, potentially causing conflicts or dissatisfaction within marriages, especially if traditional roles are challenged.

Inability to Go Back to Do Business Perceived as “Lower Socioeconomic”:

Entrepreneurial Barriers: Educated individuals may feel trapped in their career paths, unable to pivot to entrepreneurship or other non-traditional roles without risking social stigma. This perception of certain businesses as “lower socioeconomic” can prevent them from pursuing potentially fulfilling and profitable ventures (World Bank).

Risk Aversion: Higher education often leads to risk aversion, where individuals prefer the stability of employment over the uncertainties of starting a business. This conservative approach can limit their opportunities for significant QoL improvements through entrepreneurship.

Servitude of Service Jobs Taken by Educated Individuals:

Job Dissatisfaction: Many graduates find themselves in service-oriented jobs that may not align with their education or career aspirations. The servitude nature of these jobs, coupled with the disconnect from their education, can lead to job dissatisfaction and lower life satisfaction.

Economic Pressure: The necessity to repay student loans and meet living expenses often forces educated individuals into jobs that do not utilize their full potential, leading to feelings of underachievement and frustration.

Reducing Chances of Entrepreneurship:

Socioeconomic Barriers: Entrepreneurship increasingly appears to be dominated by individuals with access to significant capital, often from affluent backgrounds. This reduces the chances for those from less privileged backgrounds, even if they are highly educated, to pursue entrepreneurial opportunities (World Bank).

VC and Networking Challenges: Access to venture capital and entrepreneurial networks is often limited to those with the right connections or backgrounds, making it difficult for highly educated individuals without these advantages to succeed in starting their own businesses.

Realization of Index Investing (e.g., SPY) for QoL Satisfaction:

Financial Independence: As individuals realize the time and stress associated with traditional employment, many are turning to passive investing strategies, such as investing in index funds (e.g., SPY), to achieve financial independence and improve QoL. This shift reflects a growing understanding that financial security can be achieved through means other than prolonged education and employment (World Bank).

Shift in Priorities: The realization that passive income (and/or wealth creation) from investments can provide a more stable and less stressful life has led many to question the traditional emphasis on education as the primary path to a better QoL.

Education for Inclusion in “Cosy Clubs” Rather Than Knowledge:

Networking and Social Capital: Increasingly, education is seen as a means to gain entry into exclusive professional networks (e.g., MBA, IB, VC, PE) rather than purely for knowledge acquisition. This shift has implications for QoL, as the primary value of education becomes social capital rather than personal or intellectual development (Our World in Data).

Decline in Knowledge-Based QoL: As access to knowledge becomes more democratized through the internet, the direct impact of education on QoL through knowledge acquisition has diminished. The focus on networking rather than knowledge challenges the traditional notion of education as a means to improve QoL through intellectual growth.

1. Long Years in Education, Job Stability and Income Mobility:

Traditionally, more years in education have been strongly associated with higher income and better job stability. However, several factors, including M0/1/2/Consumer inflation and technological disruption, have weakened this association in recent years.

Career Sharpe Ratio — Formal Definition

Expected real earnings

\[ E_t = \frac{W_t}{P_t / 100} \cdot (1 - u_t) \]

where:

\[ \begin{aligned} W_t & = \text{nominal median earnings at time } t \\ P_t & = \text{price level (CPI index, base } 100) \\ u_t & = \text{unemployment rate at time } t \end{aligned} \]

Career return (growth)

\[ r_t = \ln(E_t) - \ln(E_{t-1}) \]

Career Sharpe Ratio

Let:

\[ \mu_r = \mathbb{E}[r_t] \]

\[ \sigma_r = \sqrt{\mathbb{V}[r_t]} \]

Let ( k ) denote the number of periods per year (e.g., ( k = 4 ) for quarterly data).

\[ \text{CareerSharpe} = \frac{k \, \mu_r}{\sqrt{k} \, \sigma_r} \]

or equivalently,

\[ \text{CareerSharpe} = \frac{\mathbb{E}[r_t]}{\sqrt{\mathbb{V}[r_t]}} \cdot \sqrt{k} \]

Interpretation

\[ \text{CareerSharpe} > 0 \;\Rightarrow\; \text{growth dominates volatility (stable career)} \]

\[ \text{CareerSharpe} = 0 \;\Rightarrow\; \text{growth equals instability} \]

\[ \text{CareerSharpe} < 0 \;\Rightarrow\; \text{volatility dominates growth (fragile career)} \]

Individual-level extension

\[ \text{CareerSharpe}_i = \frac{\mathbb{E}[r_{i,t}]}{\sqrt{\mathbb{V}[r_{i,t}]}} \cdot \sqrt{k} \]

EARNING_FRED_SERIES = {

# ------------------------------------------------------------------

# Median usual weekly nominal earnings

# Full-time wage & salary workers, age 25+

# Quarterly

# ------------------------------------------------------------------

"earn_lt_hs_q": "LEU0252920700Q", # Less than HS diploma, 25+

"earn_hs_q": "LEU0252917300Q", # HS graduates, no college, 25+

"earn_some_q": "LEU0254929400Q", # Some college or associate degree, 25+

"earn_ba_q": "LEU0252919100Q", # Bachelor's degree only, 25+

"earn_adv_q": "LEU0252919700Q", # Advanced degree, 25+

# ------------------------------------------------------------------

# Unemployment rates

# Age 25+, monthly, seasonally adjusted

# ------------------------------------------------------------------

"unemp_lt_hs_m": "LNS14027659", # Less than HS, 25+

"unemp_hs_m": "LNS14027660", # HS graduates, no college, 25+

"unemp_some_m": "LNS14027689", # Some college or associate degree, 25+

"unemp_ba_m": "CGRA2024", # Bachelor's degree, 25+

"unemp_adv_m": "ADVRA25", # Advanced degree (Master's+), 25+

# ------------------------------------------------------------------

# Inflation

# ------------------------------------------------------------------

"cpi_m": "CPIAUCSL", # CPI-U, monthly, seasonally adjusted

}import numpy as np

import pandas as pd

from pandas_datareader import data as pdr

def fetch_fred(series_id: str, start="2000-01-01"):

s = pdr.DataReader(series_id, "fred", start=start)

s.columns = [series_id]

return s

def annualized_sharpe(log_returns: pd.Series, periods_per_year=4) -> float:

lr = log_returns.dropna()

if len(lr) < 8:

return np.nan

mu = lr.mean() * periods_per_year

sig = lr.std(ddof=1) * np.sqrt(periods_per_year)

return float(mu / sig) if sig > 0 else np.nan

def to_quarterly_period_mean(monthly: pd.Series) -> pd.Series:

"""

Convert a monthly DatetimeIndex series to quarterly series indexed by PeriodIndex('Q'),

using mean within quarter.

"""

q = monthly.copy()

q.index = q.index.to_period("Q")

return q.groupby(level=0).mean()

def to_quarterly_period_last(monthly: pd.Series) -> pd.Series:

"""

Sometimes you may prefer end-of-quarter value instead of mean.

"""

q = monthly.copy()

q.index = q.index.to_period("Q")

return q.groupby(level=0).last()

def to_quarterly_period_from_quarterly(quarterly: pd.Series) -> pd.Series:

"""

Convert quarterly DatetimeIndex (often quarter-start dates on FRED) to PeriodIndex('Q').

"""

q = quarterly.copy()

q.index = q.index.to_period("Q")

return q

def career_sharpe_for_group_period(

earn_q: pd.Series, # quarterly earnings (nominal weekly)

unemp_m: pd.Series, # monthly unemployment rate in %

cpi_m: pd.Series, # monthly CPI index

use_cpi_mean=True,

use_unemp_mean=True,

) -> pd.DataFrame:

# --- Convert to quarterly PeriodIndex('Q') ---

earn_qp = to_quarterly_period_from_quarterly(earn_q)

unemp_qp = to_quarterly_period_mean(unemp_m) if use_unemp_mean else to_quarterly_period_last(unemp_m)

unemp_qp = unemp_qp / 100.0 # % -> fraction

cpi_qp = to_quarterly_period_mean(cpi_m) if use_cpi_mean else to_quarterly_period_last(cpi_m)

# --- Align on common quarters ---

idx = earn_qp.dropna().index.intersection(unemp_qp.dropna().index).intersection(cpi_qp.dropna().index)

earn_qp = earn_qp.loc[idx]

unemp_qp = unemp_qp.loc[idx]

cpi_qp = cpi_qp.loc[idx]

# --- Compute proxy expected real earnings ---

real_weekly = earn_qp / (cpi_qp / 100.0)

expected_real_weekly = real_weekly * (1.0 - unemp_qp)

# Quarterly log returns

r = np.log(expected_real_weekly).diff()

out = pd.DataFrame({

"earn_nominal_weekly": earn_qp,

"cpi": cpi_qp,

"unemp_rate": unemp_qp,

"real_weekly": real_weekly,

"expected_real_weekly": expected_real_weekly,

"log_return_qoq": r,

})

out.attrs["career_sharpe"] = annualized_sharpe(out["log_return_qoq"])

return out

def run_all_fred_series_for_career_sharpe(FRED_SERIES, start="2000-01-01"):

earnings = {

"lt_hs": fetch_fred(FRED_SERIES["earn_lt_hs_q"], start).iloc[:, 0],

"hs": fetch_fred(FRED_SERIES["earn_hs_q"], start).iloc[:, 0],

"some": fetch_fred(FRED_SERIES["earn_some_q"], start).iloc[:, 0],

"ba": fetch_fred(FRED_SERIES["earn_ba_q"], start).iloc[:, 0],

"adv": fetch_fred(FRED_SERIES["earn_adv_q"], start).iloc[:, 0],

}

unemp = {

"lt_hs": fetch_fred(FRED_SERIES["unemp_lt_hs_m"], start).iloc[:, 0],

"hs": fetch_fred(FRED_SERIES["unemp_hs_m"], start).iloc[:, 0],

"some": fetch_fred(FRED_SERIES["unemp_some_m"], start).iloc[:, 0],

"ba": fetch_fred(FRED_SERIES["unemp_ba_m"], start).iloc[:, 0],

}

cpi = fetch_fred(FRED_SERIES["cpi_m"], start).iloc[:, 0]

# Advanced-degree unemployment fallback

try:

unemp["adv"] = fetch_fred(FRED_SERIES["unemp_adv_m"], start).iloc[:, 0]

except Exception:

unemp["adv"] = fetch_fred("LNS14027662", start).iloc[:, 0]

results = {}

rows = []

for k in ["lt_hs", "hs", "some", "ba", "adv"]:

df = career_sharpe_for_group_period(

earn_q=earnings[k],

unemp_m=unemp[k],

cpi_m=cpi,

use_cpi_mean=True,

use_unemp_mean=True,

)

results[k] = df

lr = df["log_return_qoq"].dropna()

rows.append({

"education_group": k,

"career_sharpe": df.attrs["career_sharpe"],

"start_q": str(df.index.min()) if not df.empty else None,

"end_q": str(df.index.max()) if not df.empty else None,

"n_quarters": int(lr.shape[0]),

})

sharpe_table = pd.DataFrame(rows).sort_values("career_sharpe", ascending=False)

return sharpe_table, resultssharpe_table, results = run_all_fred_series_for_career_sharpe(EARNING_FRED_SERIES, start=start_date_str)

print(sharpe_table.to_string(index=False))education_group career_sharpe start_q end_q n_quarters

adv 0.026205 2000Q1 2025Q3 102

lt_hs 0.024898 2000Q1 2025Q3 102

hs 0.017300 2000Q1 2025Q3 102

some -0.026485 2000Q1 2025Q3 102

ba -0.031516 2000Q1 2025Q3 102results["ba"].tail()| earn_nominal_weekly | cpi | unemp_rate | real_weekly | expected_real_weekly | log_return_qoq | |

|---|---|---|---|---|---|---|

| DATE | ||||||

| 2024Q3 | 1533 | 314.182667 | 0.082667 | 487.932710 | 447.596939 | -0.030950 |

| 2024Q4 | 1547 | 316.538667 | 0.056667 | 488.723863 | 461.029511 | 0.029569 |

| 2025Q1 | 1603 | 319.492000 | 0.064667 | 501.734003 | 469.288537 | 0.017756 |

| 2025Q2 | 1559 | 320.800333 | 0.057667 | 485.972064 | 457.947675 | -0.024463 |

| 2025Q3 | 1580 | 323.288000 | 0.091333 | 488.728317 | 444.091130 | -0.030725 |

EDU_YEARS_MAP = {

"lt_hs": 10,

"hs": 12,

"some": 14,

"ba": 16,

"adv": 18,

}

def rolling_career_sharpe_series(df, window=20, periods_per_year=4):

"""

Rolling Career Sharpe from a group's df (must contain log_return_qoq).

Annualized mean / annualized std with quarterly periods.

"""

r = df["log_return_qoq"]

mu = r.rolling(window).mean() * periods_per_year

sig = r.rolling(window).std(ddof=1) * np.sqrt(periods_per_year)

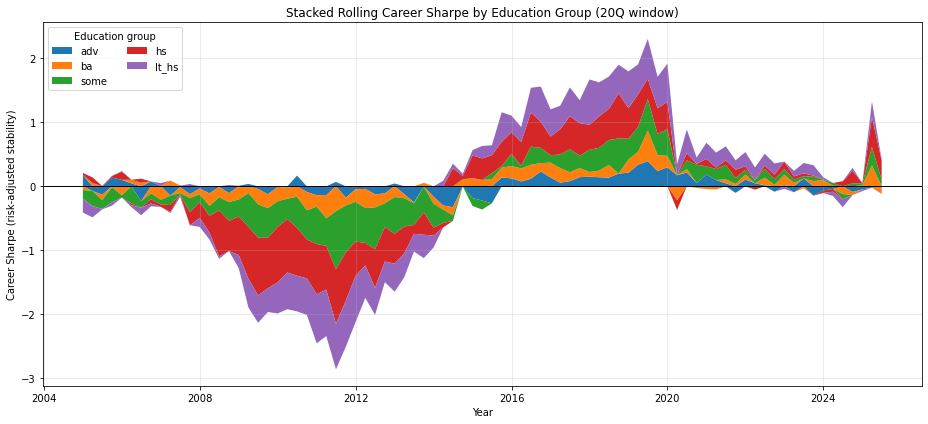

return mu / sigdef plot_stacked_rolling_career_sharpe_semantic(results, window=20):

"""

Fixed semantic order (education ladder), with higher education closer to the zero line.

Uses consistent colors for the same group above and below zero.

"""

# --- Fixed semantic order (higher ed near zero) ---

groups = ["adv", "ba", "some", "hs", "lt_hs"] # fixed ladder order

# ---- Build aligned DataFrame of rolling Sharpe ----

sharpe_series = []

for k in groups:

df = results.get(k)

if df is None or df.empty:

continue

mu = df["log_return_qoq"].rolling(window).mean() * 4

sig = df["log_return_qoq"].rolling(window).std() * np.sqrt(4)

sharpe_series.append((mu / sig).rename(k))

sharpe_df = pd.concat(sharpe_series, axis=1).dropna(how="all")

sharpe_df.index = sharpe_df.index.to_timestamp()

# Ensure all groups exist & order is preserved

groups_present = [g for g in groups if g in sharpe_df.columns]

sharpe_df = sharpe_df[groups_present]

# ---- Split into positive and negative parts ----

pos = sharpe_df.clip(lower=0)

neg = sharpe_df.clip(upper=0)

# ---- Consistent colors per group ----

cmap = plt.get_cmap("tab10")

color_map = {g: cmap(i % 10) for i, g in enumerate(groups_present)}

colors = [color_map[g] for g in groups_present]

# ---- Plot ----

plt.figure(figsize=(13, 6))

# Positive stack

plt.stackplot(

pos.index,

[pos[g].values for g in groups_present],

labels=groups_present,

colors=colors,

alpha=1.0

)

# Negative stack (same order, same colors)

plt.stackplot(

neg.index,

[neg[g].values for g in groups_present],

colors=colors,

alpha=1.0

)

plt.axhline(0, color="black", lw=1)

plt.title(f"Stacked Rolling Career Sharpe by Education Group ({window}Q window)")

plt.ylabel("Career Sharpe (risk-adjusted stability)")

plt.xlabel("Year")

plt.legend(loc="upper left", title="Education group", ncol=2)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

# Usage:

plot_stacked_rolling_career_sharpe_semantic(results, window=20)

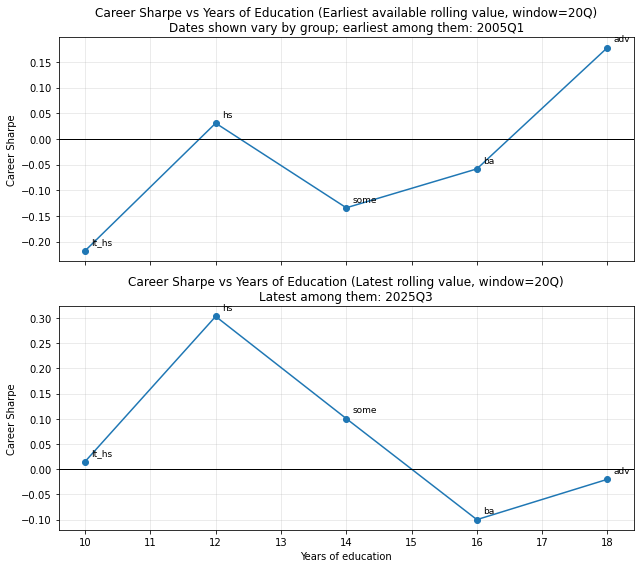

def plot_sharpe_vs_edu_at_sample_ends(results, edu_years_map, window=20):

"""

Two-row plot (shared X axis: years of education):

Row 1: Sharpe at earliest available date (first non-NaN rolling value per group)

Row 2: Sharpe at latest available date (last rolling value per group)

"""

rows_early = []

rows_late = []

for group, df in results.items():

if df is None or df.empty or group not in edu_years_map:

continue

s = rolling_career_sharpe_series(df, window=window).dropna()

if s.empty:

continue

years = edu_years_map[group]

# Earliest defined rolling Sharpe (after window)

early_date = s.index[0]

early_val = float(s.iloc[0])

# Latest rolling Sharpe (end of sample)

late_date = s.index[-1]

late_val = float(s.iloc[-1])

rows_early.append({

"group": group,

"years_education": years,

"career_sharpe": early_val,

"date": early_date

})

rows_late.append({

"group": group,

"years_education": years,

"career_sharpe": late_val,

"date": late_date

})

df_early = pd.DataFrame(rows_early).sort_values("years_education")

df_late = pd.DataFrame(rows_late).sort_values("years_education")

# If you want the "early" and "late" dates to be common across groups,

# you can display the range here:

early_dates = df_early["date"].tolist()

late_dates = df_late["date"].tolist()

fig, axes = plt.subplots(nrows=2, ncols=1, figsize=(9, 8), sharex=True)

# ---- Row 1: earliest ----

axes[0].plot(df_early["years_education"], df_early["career_sharpe"], marker="o")

axes[0].axhline(0, color="black", lw=1)

axes[0].set_title(

f"Career Sharpe vs Years of Education (Earliest available rolling value, window={window}Q)\n"

f"Dates shown vary by group; earliest among them: {min(early_dates)}"

)

axes[0].set_ylabel("Career Sharpe")

axes[0].grid(alpha=0.3)

for _, r in df_early.iterrows():

axes[0].annotate(r["group"], (r["years_education"], r["career_sharpe"]),

textcoords="offset points", xytext=(6, 6), fontsize=9)

# ---- Row 2: latest ----

axes[1].plot(df_late["years_education"], df_late["career_sharpe"], marker="o")

axes[1].axhline(0, color="black", lw=1)

axes[1].set_title(

f"Career Sharpe vs Years of Education (Latest rolling value, window={window}Q)\n"

f"Latest among them: {max(late_dates)}"

)

axes[1].set_ylabel("Career Sharpe")

axes[1].set_xlabel("Years of education")

axes[1].grid(alpha=0.3)

for _, r in df_late.iterrows():

axes[1].annotate(r["group"], (r["years_education"], r["career_sharpe"]),

textcoords="offset points", xytext=(6, 6), fontsize=9)

plt.tight_layout()

plt.show()

return df_early, df_late

# Usage:

df_early, df_late = plot_sharpe_vs_edu_at_sample_ends(results, EDU_YEARS_MAP, window=20)

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import matplotlib.colors as mcolors

from pandas_datareader import data as pdr

def fetch_us_recessions(start="1990-01-01"):

"""

Fetch US recession indicator (USREC) from FRED.

1 = recession, 0 = expansion.

"""

rec = pdr.DataReader("USREC", "fred", start)

rec.index = pd.to_datetime(rec.index)

return rec

def recession_intervals(usrec: pd.DataFrame):

"""

Convert monthly USREC series into a list of (start, end) timestamps.

"""

rec = usrec["USREC"]

intervals = []

in_rec = False

start = None

for date, val in rec.items():

if val == 1 and not in_rec:

start = date

in_rec = True

elif val == 0 and in_rec:

intervals.append((start, date))

in_rec = False

if in_rec:

intervals.append((start, rec.index[-1]))

return intervals

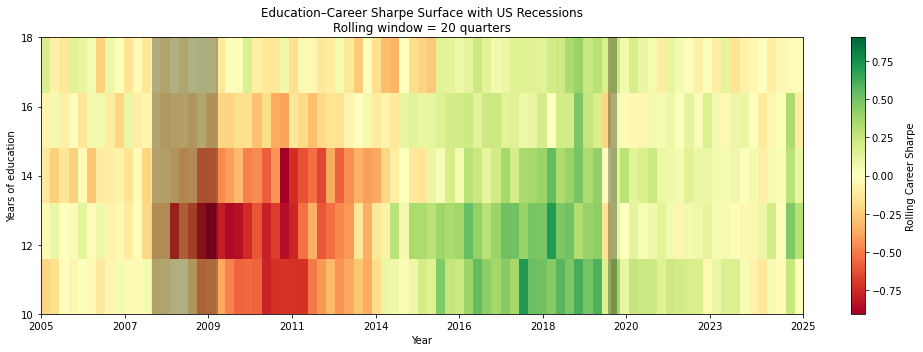

def plot_edu_sharpe_heatmap_with_recessions(

results,

edu_years_map,

window=20,

rec_start="1990-01-01"

):

# ---- Build panel (same as before) ----

panel = build_edu_sharpe_panel(results, edu_years_map, window=window)

Z = np.ma.masked_invalid(panel.T.values)

years = panel.columns.values

times = panel.index.values

# ---- Zero-centered normalization ----

vmax = np.nanmax(np.abs(Z))

norm = mcolors.TwoSlopeNorm(vmin=-vmax, vcenter=0.0, vmax=vmax)

# ---- Fetch recessions ----

usrec = fetch_us_recessions(start=rec_start)

rec_intervals = recession_intervals(usrec)

# ---- Plot ----

plt.figure(figsize=(14, 5))

plt.imshow(

Z,

aspect="auto",

origin="lower",

interpolation="nearest",

cmap="RdYlGn",

norm=norm,

extent=[0, len(times) - 1, years.min(), years.max()]

)

# X ticks (years)

n_xticks = min(10, len(times))

xtick_pos = np.linspace(0, len(times) - 1, n_xticks).astype(int)

xtick_lbl = [pd.to_datetime(times[i]).strftime("%Y") for i in xtick_pos]

plt.xticks(xtick_pos, xtick_lbl)

# Y ticks (education years)

plt.yticks(years, [str(int(y)) for y in years])

# ---- Overlay recession bands ----

time_index = pd.to_datetime(times)

for start, end in rec_intervals:

# find indices overlapping the heatmap time range

if end < time_index.min() or start > time_index.max():

continue

x0 = np.searchsorted(time_index, start, side="left")

x1 = np.searchsorted(time_index, end, side="right")

plt.axvspan(

x0, x1,

color="black",

alpha=0.3, # subtle but visible

lw=0

)

cbar = plt.colorbar()

cbar.set_label("Rolling Career Sharpe")

plt.title(

f"Education–Career Sharpe Surface with US Recessions\n"

f"Rolling window = {window} quarters"

)

plt.xlabel("Year")

plt.ylabel("Years of education")

plt.tight_layout()

plt.show()

return panel

plot_edu_sharpe_heatmap_with_recessions(

results,

EDU_YEARS_MAP,

window=20,

rec_start="1990-01-01"

)

| 10 | 12 | 14 | 16 | 18 | |

|---|---|---|---|---|---|

| DATE | |||||

| 2005-01-01 | -0.217867 | 0.030670 | -0.134112 | -0.058386 | 0.177880 |

| 2005-04-01 | -0.176164 | 0.088045 | -0.236736 | 0.051427 | -0.072408 |

| 2005-07-01 | -0.007828 | 0.005134 | -0.137005 | -0.082290 | -0.133007 |

| 2005-10-01 | -0.054053 | 0.026606 | -0.236067 | -0.012380 | 0.135676 |

| 2006-01-01 | 0.011318 | 0.126577 | -0.034653 | -0.141063 | 0.101021 |

| ... | ... | ... | ... | ... | ... |

| 2024-07-01 | -0.122012 | 0.078718 | -0.081831 | -0.117491 | -0.003857 |

| 2024-10-01 | 0.044885 | 0.197410 | 0.045686 | -0.050311 | -0.087999 |

| 2025-01-01 | -0.026605 | 0.008222 | 0.026629 | 0.015947 | -0.048712 |

| 2025-04-01 | 0.243602 | 0.465019 | 0.290055 | 0.326661 | -0.021351 |

| 2025-07-01 | 0.015073 | 0.303110 | 0.100364 | -0.100123 | -0.020048 |

83 rows × 5 columns

Observation from the chart

Education =/= insurance anymore

Higher education:

- Raises mean income

- Raises volatility more

- Lowers Career Sharpe

Across 2000–2025, risk-adjusted career outcomes in the US show no monotonic relationship with years of education; instead, education cohorts move together across macro regimes, with mid-to-upper education levels exhibiting the greatest downside during shocks and no group offering persistent career stability.

It’s Inflation !

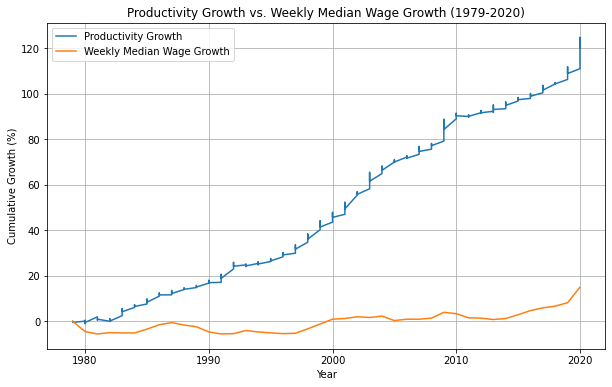

2. Reducing Compensation Given a Productivity Level

M0/1/2 Inflation and Real Wages: The increase in M2 money supply has contributed to inflation, which in turn has eroded the purchasing power of wages. While nominal wages might rise, real wages—adjusted for inflation—have stagnated or even declined for many workers, particularly those in jobs traditionally associated with higher education.

Data Evidence: Studies such as those from the Federal Reserve Bank of St. Louis have shown that while M2 has increased significantly, the growth in real wages has not kept pace, particularly after the 2008 financial crisis (St. Louis Fed).

Example: The Economic Policy Institute found that between 1979 and 2020, the median worker’s wages grew by only 15.1% when adjusted for inflation, while productivity increased by 61.8%. This decoupling suggests that higher education does not necessarily lead to proportionate income growth in an inflationary environment.

Download Productivity data

headers = {

"User-Agent": "Mozilla/5.0 (Macintosh; Intel Mac OS X 10_15_7) AppleWebKit/537.36 (KHTML, like Gecko) Chrome/127.0.0.0 Safari/537.36"

}

productivity_url = "https://download.bls.gov/pub/time.series/pr/pr.data.1.AllData"

data = requests.get(productivity_url, headers=headers).text

productivity_data = pd.read_csv(StringIO(data), sep="\t")

productivity_data.columns = ['series_id', 'year', 'period', 'value','footnote_codes']

productivity_data['series_id'] = productivity_data['series_id'].str.strip()

productivity_data['period'] = productivity_data['period'].str.strip()

#productivity_data.info()

# Step 2: Process the productivity data

# Filtering for relevant data (example uses a hypothetical series code PRS85006093 for nonfarm business productivity)

productivity_data = productivity_data[(productivity_data['series_id'] == 'PRS85006093') & (productivity_data['year'] >= start_date.year)]

productivity_data = productivity_data[['year', 'value']].rename(columns={'value': 'Productivity_Index'})

productivity_data.head()| year | Productivity_Index | |

|---|---|---|

| 45473 | 1979 | 49.615 |

| 45474 | 1979 | 49.523 |

| 45475 | 1979 | 49.463 |

| 45476 | 1979 | 49.405 |

| 45477 | 1979 | 49.360 |

Download Median Wage Data

import pandas_datareader as pdr

from datetime import datetime

# LEU0252881600Q: Median usual weekly real earnings: Wage and salary workers: 16 years and over

wage_data = pdr.get_data_fred('LEU0252881600Q', start=datetime(1979, 1, 1), end=datetime(2020, 12, 31))

# Preview the data

wage_data = wage_data.groupby(wage_data.index.year)["LEU0252881600Q"].median()

wage_data = wage_data.reset_index()

# Step 3: Process the wage data

# Assuming the data is already in the right format

wage_data = wage_data[wage_data['DATE'] >= 1979]

wage_data = wage_data[['DATE', 'LEU0252881600Q']].rename(columns={'DATE':'year', 'LEU0252881600Q': 'Weekly_Median_Wage'})

wage_data.head()| year | Weekly_Median_Wage | |

|---|---|---|

| 0 | 1979 | 331.0 |

| 1 | 1980 | 316.0 |

| 2 | 1981 | 312.5 |

| 3 | 1982 | 314.5 |

| 4 | 1983 | 314.0 |

# Step 4: Merge the datasets on the year

merged_data = pd.merge(productivity_data, wage_data, left_on='year', right_on='year')

merged_data.head()| year | Productivity_Index | Weekly_Median_Wage | |

|---|---|---|---|

| 0 | 1979 | 49.615 | 331.0 |

| 1 | 1979 | 49.523 | 331.0 |

| 2 | 1979 | 49.463 | 331.0 |

| 3 | 1979 | 49.405 | 331.0 |

| 4 | 1979 | 49.360 | 331.0 |

# Step 5: Calculate cumulative growth

base_productivity = merged_data['Productivity_Index'].iloc[0]

base_wage = merged_data['Weekly_Median_Wage'].iloc[0]

merged_data['Productivity_Growth'] = ((merged_data['Productivity_Index'] - base_productivity) / base_productivity) * 100

merged_data['Weekly_Median_Wage_Growth'] = ((merged_data['Weekly_Median_Wage'] - base_wage) / base_wage) * 100

# Step 6: Plot the data

plt.figure(figsize=(10, 6))

plt.plot(merged_data['year'], merged_data['Productivity_Growth'], label='Productivity Growth')

plt.plot(merged_data['year'], merged_data['Weekly_Median_Wage_Growth'], label='Weekly Median Wage Growth')

plt.title('Productivity Growth vs. Weekly Median Wage Growth (1979-2020)')

plt.xlabel('Year')

plt.ylabel('Cumulative Growth (%)')

plt.legend()

plt.grid(True)

plt.show()

# Display the final growth rates

print(f"Productivity Growth (1979-2020): {merged_data['Productivity_Growth'].iloc[-1]:.2f}%")

print(f"Weekly Median Wage Growth (1979-2020): {merged_data['Weekly_Median_Wage_Growth'].iloc[-1]:.2f}%")

Productivity Growth (1979-2020): 120.07%

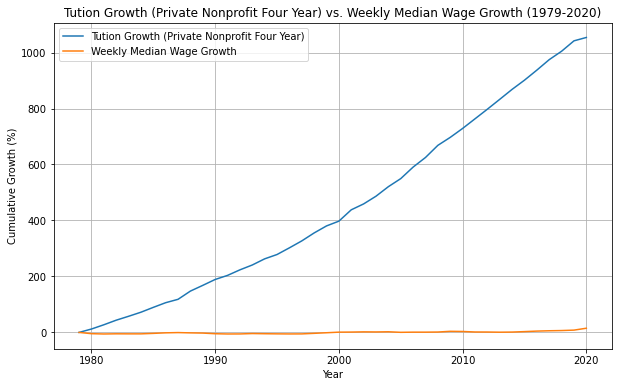

Weekly Median Wage Growth (1979-2020): 14.95%Impact of M2 Inflation: Rising Costs of Living and Education

Education Costs: The cost of education has risen significantly, outpacing inflation and wage growth. As M2 inflation contributes to the overall increase in the cost of living, students graduate with higher levels of debt, which diminishes the net financial returns of their education.

Case Study: According to the College Board, the average cost of tuition and fees at private four-year institutions in the U.S. has more than doubled since 2000, while wages have not kept pace with these increases

Data Source: https://research.collegeboard.org/media/xlsx/trends-college-pricing-excel-data-2023.xlsx

tution_data = pd.read_csv("data/tuition_private_4yr_current_dollars_final_cleaned.csv")

tution_data.columns = ['year', 'Private_Nonprofit_Four_Year']

tution_data.head()| year | Private_Nonprofit_Four_Year | |

|---|---|---|

| 0 | 1971 | 1830.0 |

| 1 | 1972 | 1950.0 |

| 2 | 1973 | 2050.0 |

| 3 | 1974 | 2130.0 |

| 4 | 1975 | 2290.0 |

# Step 4: Merge the datasets on the year

merged_data = pd.merge(tution_data, wage_data, left_on='year', right_on='year')

merged_data.head()| year | Private_Nonprofit_Four_Year | Weekly_Median_Wage | |

|---|---|---|---|

| 0 | 1979 | 3230.0 | 331.0 |

| 1 | 1980 | 3620.0 | 316.0 |

| 2 | 1981 | 4110.0 | 312.5 |

| 3 | 1982 | 4640.0 | 314.5 |

| 4 | 1983 | 5090.0 | 314.0 |

# Step 5: Calculate cumulative growth

base_tution = merged_data['Private_Nonprofit_Four_Year'].iloc[0]

base_wage = merged_data['Weekly_Median_Wage'].iloc[0]

merged_data['Tution_Growth'] = ((merged_data['Private_Nonprofit_Four_Year'] - base_tution) / base_tution) * 100

merged_data['Weekly_Median_Wage_Growth'] = ((merged_data['Weekly_Median_Wage'] - base_wage) / base_wage) * 100

# Step 6: Plot the data

plt.figure(figsize=(10, 6))

plt.plot(merged_data['year'], merged_data['Tution_Growth'], label='Tution Growth (Private Nonprofit Four Year)')

plt.plot(merged_data['year'], merged_data['Weekly_Median_Wage_Growth'], label='Weekly Median Wage Growth')

plt.title('Tution Growth (Private Nonprofit Four Year) vs. Weekly Median Wage Growth (1979-2020)')

plt.xlabel('Year')

plt.ylabel('Cumulative Growth (%)')

plt.legend()

plt.grid(True)

plt.show()

# Display the final growth rates

print(f"Tution Growth (Private Nonprofit Four Year) (1979-): {merged_data['Tution_Growth'].iloc[-1]:.2f}%")

print(f"Weekly Median Wage Growth (1979-): {merged_data['Weekly_Median_Wage_Growth'].iloc[-1]:.2f}%")

Tution Growth (Private Nonprofit Four Year) (1979-): 1053.87%

Weekly Median Wage Growth (1979-): 14.95%Now let’s explore how Tution Growth and M2 Inflation are related.

Tution Growth and M2 Inflation

# Fetch M2 Money Stock data

m2_supply = web.DataReader('M2SL', 'fred', start_date, end_date)

m2_supply = m2_supply.groupby(m2_supply.index.year)["M2SL"].mean()

m2_supply.dropna()

m2_supply = pd.DataFrame(data={

'year': m2_supply.index,

'm2sl': m2_supply.values

})

m2_supply.reset_index()

m2_supply.head(5)| year | m2sl | |

|---|---|---|

| 0 | 1979 | 1425.666667 |

| 1 | 1980 | 1540.183333 |

| 2 | 1981 | 1679.291667 |

| 3 | 1982 | 1830.925000 |

| 4 | 1983 | 2054.466667 |

tution_m2sl_merged_data = pd.merge(tution_data, m2_supply, left_on='year', right_on='year')

tution_m2sl_merged_data.head()| year | Private_Nonprofit_Four_Year | m2sl | |

|---|---|---|---|

| 0 | 1979 | 3230.0 | 1425.666667 |

| 1 | 1980 | 3620.0 | 1540.183333 |

| 2 | 1981 | 4110.0 | 1679.291667 |

| 3 | 1982 | 4640.0 | 1830.925000 |

| 4 | 1983 | 5090.0 | 2054.466667 |

# Perform Granger Causality Test

granger_test = grangercausalitytests(tution_m2sl_merged_data[['Private_Nonprofit_Four_Year', 'm2sl']],

maxlag=12,

verbose=True)

Granger Causality

number of lags (no zero) 1

ssr based F test: F=0.0591 , p=0.8092 , df_denom=41, df_num=1

ssr based chi2 test: chi2=0.0634 , p=0.8012 , df=1

likelihood ratio test: chi2=0.0634 , p=0.8013 , df=1

parameter F test: F=0.0591 , p=0.8092 , df_denom=41, df_num=1

Granger Causality

number of lags (no zero) 2

ssr based F test: F=0.2816 , p=0.7561 , df_denom=38, df_num=2

ssr based chi2 test: chi2=0.6373 , p=0.7271 , df=2

likelihood ratio test: chi2=0.6327 , p=0.7288 , df=2

parameter F test: F=0.2816 , p=0.7561 , df_denom=38, df_num=2

Granger Causality

number of lags (no zero) 3

ssr based F test: F=11.8657 , p=0.0000 , df_denom=35, df_num=3

ssr based chi2 test: chi2=42.7165 , p=0.0000 , df=3

likelihood ratio test: chi2=29.4689 , p=0.0000 , df=3

parameter F test: F=11.8657 , p=0.0000 , df_denom=35, df_num=3

Granger Causality

number of lags (no zero) 4

ssr based F test: F=8.6750 , p=0.0001 , df_denom=32, df_num=4

ssr based chi2 test: chi2=44.4595 , p=0.0000 , df=4

likelihood ratio test: chi2=30.1133 , p=0.0000 , df=4

parameter F test: F=8.6750 , p=0.0001 , df_denom=32, df_num=4

Granger Causality

number of lags (no zero) 5

ssr based F test: F=6.3667 , p=0.0004 , df_denom=29, df_num=5

ssr based chi2 test: chi2=43.9086 , p=0.0000 , df=5

likelihood ratio test: chi2=29.6339 , p=0.0000 , df=5

parameter F test: F=6.3667 , p=0.0004 , df_denom=29, df_num=5

Granger Causality

number of lags (no zero) 6

ssr based F test: F=6.0540 , p=0.0005 , df_denom=26, df_num=6

ssr based chi2 test: chi2=54.4860 , p=0.0000 , df=6

likelihood ratio test: chi2=34.0958 , p=0.0000 , df=6

parameter F test: F=6.0540 , p=0.0005 , df_denom=26, df_num=6

Granger Causality

number of lags (no zero) 7

ssr based F test: F=5.2112 , p=0.0012 , df_denom=23, df_num=7

ssr based chi2 test: chi2=60.2682 , p=0.0000 , df=7

likelihood ratio test: chi2=36.1043 , p=0.0000 , df=7

parameter F test: F=5.2112 , p=0.0012 , df_denom=23, df_num=7

Granger Causality

number of lags (no zero) 8

ssr based F test: F=4.1960 , p=0.0044 , df_denom=20, df_num=8

ssr based chi2 test: chi2=62.1003 , p=0.0000 , df=8

likelihood ratio test: chi2=36.4529 , p=0.0000 , df=8

parameter F test: F=4.1960 , p=0.0044 , df_denom=20, df_num=8

Granger Causality

number of lags (no zero) 9

ssr based F test: F=4.0155 , p=0.0066 , df_denom=17, df_num=9

ssr based chi2 test: chi2=76.5310 , p=0.0000 , df=9

likelihood ratio test: chi2=41.0296 , p=0.0000 , df=9

parameter F test: F=4.0155 , p=0.0066 , df_denom=17, df_num=9

Granger Causality

number of lags (no zero) 10

ssr based F test: F=3.1079 , p=0.0262 , df_denom=14, df_num=10

ssr based chi2 test: chi2=77.6984 , p=0.0000 , df=10

likelihood ratio test: chi2=40.9278 , p=0.0000 , df=10

parameter F test: F=3.1079 , p=0.0262 , df_denom=14, df_num=10

Granger Causality

number of lags (no zero) 11

ssr based F test: F=4.4091 , p=0.0105 , df_denom=11, df_num=11

ssr based chi2 test: chi2=149.9104, p=0.0000 , df=11

likelihood ratio test: chi2=57.3950 , p=0.0000 , df=11

parameter F test: F=4.4091 , p=0.0105 , df_denom=11, df_num=11

Granger Causality

number of lags (no zero) 12

ssr based F test: F=13.2302 , p=0.0005 , df_denom=8, df_num=12

ssr based chi2 test: chi2=654.8936, p=0.0000 , df=12

likelihood ratio test: chi2=100.2252, p=0.0000 , df=12

parameter F test: F=13.2302 , p=0.0005 , df_denom=8, df_num=12/Users/dbose/anaconda3/envs/py-data/lib/python3.8/site-packages/statsmodels/tsa/stattools.py:1545: FutureWarning: verbose is deprecated since functions should not print results

warnings.warn(The Granger causality tests provide strong evidence that changes in the M2 money supply (M2SL) do indeed cause changes in the cost of tuition at Private Nonprofit Four-Year institutions, particularly when considering lags 3 through 12. The most significant causal effects are observed around lags 3-6, with some weakening around lags 7-10, and a resurgence at higher lags (lag 12). This analysis suggests that M2SL is a significant predictor of tuition costs over various lag periods, implying that changes in the money supply could have a delayed impact on educational costs.

Student Debt:

Federal Reserve data shows that student debt in the U.S. has skyrocketed, surpassing $1.7 trillion in 2021. This growing debt burden makes it harder for graduates to achieve financial stability, let alone upward mobility.

Impact of Technological Disruption: Automation and Job Displacement:

Tech Disruption: Technological advancements, particularly in automation and AI, have disrupted industries that traditionally offered stable employment to highly educated individuals. Jobs in fields like accounting (A), legal services (L), and even medicine (M) (LAM in acronym) are increasingly being automated, reducing the demand for highly educated workers in these areas.

Research Findings: A 2020 report by the World Economic Forum predicts that by 2025, automation will displace about 85 million jobs globally, many of which are held by individuals with higher education. This disruption challenges the stability that higher education once promised (World Bank).

Global Displacement Estimates: 400 to 800 million individuals globally could be displaced by automation and need to find new jobs by 2030. This estimate reflects the potential impact under various scenarios of automation adoption.

Occupation Shifts: 75 to 375 million workers may need to switch occupational categories and learn new skills to remain employed, depending on the speed of automation adoption. This transition represents 3% to 14% of the global workforce.

300 to 365 million new jobs could be created globally by 2030 from rising incomes and consumption, especially in emerging economies. This implies 100-435 million jobs get destroyed. This wave of automation, at least, is not a net job creator without even quantifying stress-level or level of satisfaction from those that will exist by 2030.

Example: The rise of AI tools like GPT (Generative Pre-trained Transformer) has started to replace certain tasks performed by professionals in law and finance, sectors that were once considered safe for those with advanced degrees.

Displaced workers are often forced into lower-paying jobs or must invest in learning new technologies (SaaS tools, AI/ML etc.) to remain employable, perpetuating a cycle of continual upskilling without significant wage growth.

Sources - JOBS LOST, JOBS GAINED: WORKFORCE TRANSITIONS IN A TIME OF AUTOMATION https://www.mckinsey.com/~/media/mckinsey/industries/public%20and%20social%20sector/our%20insights/what%20the%20future%20of%20work%20will%20mean%20for%20jobs%20skills%20and%20wages/mgi-jobs-lost-jobs-gained-executive-summary-december-6-2017.pdf

## Hypothesis: > Benefits of automation mostly accrue to Venture Capitalists (VCs), private equity (PEs) firms, investment funds, governments (via tax collection) and enterprises, while workers face job displacement or wage stagnation

The labor share — the fraction of economic output that accrues to workers as compensation in exchange for their labor, could be a way to measure whether the benefits of automation is accruing to labour

Source: - https://www.bls.gov/opub/mlr/2017/article/estimating-the-us-labor-share.htm

Source: - A new look at the declining labor share of income in the United States https://www.mckinsey.com/~/media/McKinsey/Featured%20Insights/Employment%20and%20Growth/A%20new%20look%20at%20the%20declining%20labor%20share%20of%20income%20in%20the%20United%20States/MGI-A-new-look-at-the-declining-labor-share-of-income-in-the-United-States.pdf

Impact of Technological Disruption: Underemployment of Graduates:

Overqualification: As more people pursue higher education, the labor market becomes saturated with degree holders, leading to underemployment. Graduates often find themselves in jobs that do not require their level of education, resulting in lower job satisfaction and income.

Statistical Evidence: The Federal Reserve Bank of New York reported that as of 2021, about 41% of recent college graduates in the U.S. were underemployed, meaning they were working in jobs that typically do not require a bachelor’s degree

52% of Graduates Underemployed: One year after graduation, 52% of college graduates with a terminal bachelor’s degree are underemployed. This rate decreases only slightly to 45% after 10 years(Talent-Disrupted-2).

STEM is not a silver bullet. While policymakers typically think of STEM (science, technology, engineering, and mathematics) programs as a sure pathway to college-level employment and high wages, the reality is more nuanced. Graduates with a bachelor’s degree in computer science, engineering, or mathematics tend to experience very low underemployment, while those with a degree in a life sciences field (e.g., biology) tend to face higher underemployment rates.

Persistence of Underemployment: 73% Remain Underemployed: A staggering 73% of those who start out underemployed remain in such positions 10 years after graduation

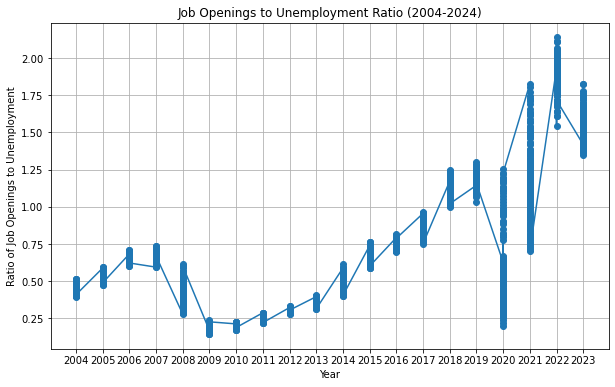

Underemployment / Unemployment, beyond skill-gap, can also indicate over-supply in labour market. One way to measure that would be to capture data about Avg Applications per Job by Sectors or ratio of Job Openings to Unemployment

Overeducation and depressive symptoms: diminishing mental health returns to education (https://sci-hub.se/10.1111/1467-9566.12039) > On the supply side, the labour market value of educational credentials inflated (Hannum and Buchmann 2005), whereas on the demand side, employers started to compete for employees with the highest credentials in order to reduce the costs of job training (Hirsch 1977, Thurow 1976). As a result, the fact that the supply of highly educated people outnumbered the demand for educated labour (Freeman 1976) led to some highly educated people ending up in jobs that actually required lower qualifications (Duncan and Hoffman 1981). This phenomenon of overeducation thus became a permanent condition for a substantial number of employees (Pritchett 2001, Rubb 2003, Vaisey 2006). At the population level the presence of overeducation is inferred from the observation of diminishing returns to tertiary education. For instance, Freeman (1976) defines overeducation as ‘a falling private rate of return to college education’ (Psacharopoulos, 1994: 1334). At the individual level it is defined as job–education mismatch, that is, when ‘the level of education acquired exceeds the level of education required to adequately perform the job’ (Wolbers 2003: 251).

Sources:

Trend in Job openings to unemployment

# BLS API Key

api_key = '36aea4409aef4dd787a9ab7107c9d232'

# Define the series IDs for job openings (JOLTS) and unemployment (UNRATE)

series_ids = {

"Job Openings": "JTS000000000000000JOL",

"Unemployment": "LNS13000000"

}

# Define the endpoint and parameters for the API request

endpoint = "https://api.bls.gov/publicAPI/v2/timeseries/data/"

headers = {

"Content-Type": "application/json"

}

# Request data for both series

data = {

"seriesid": list(series_ids.values()),

#

# NOTE:max data range can be of 20 years

#

"startyear": '2004',

"endyear": '2024',

"registrationkey": api_key

}

response = requests.post(endpoint, json=data, headers=headers)

json_data = response.json()# Extract data and create a DataFrame

series_data = {}

for series in json_data['Results']['series']:

series_id = series['seriesID']

series_name = [key for key, value in series_ids.items() if value == series_id][0]

data_points = [(item['year'], item['value']) for item in series['data']]

df = pd.DataFrame(data_points, columns=['Year', series_name])

df[series_name] = df[series_name].astype(float)

series_data[series_name] = df.set_index('Year')

# Merge the two dataframes

df_job_openings_unemployment_merged = pd.merge(series_data['Job Openings'],

series_data['Unemployment'],

left_index=True,

right_index=True)

# Calculate the ratio of Job Openings to Unemployment

df_job_openings_unemployment_merged['Job Openings to Unemployment Ratio'] = df_job_openings_unemployment_merged['Job Openings'] / df_job_openings_unemployment_merged['Unemployment']

# Plot the data

plt.figure(figsize=(10, 6))

plt.plot(df_job_openings_unemployment_merged.index,

df_job_openings_unemployment_merged['Job Openings to Unemployment Ratio'],

marker='o')

plt.title('Job Openings to Unemployment Ratio (2004-2024)')

plt.xlabel('Year')

plt.ylabel('Ratio of Job Openings to Unemployment')

plt.grid(True)

plt.show()

What’s interesting is that the ratio remained <1 (over-supply/skill-gap) till 2018, corrected during COVID and rebounded stronger. No we don’t know how much of that rebound is caused by transitioning to the “new world order”, remote/WFH tech jobs or monetary stimulus provided by government.

Trend in Job openings to unemployment - By Sectors

# Define the series IDs for job openings (JOLTS) and unemployment for various sectors

# https://www.bls.gov/help/hlpforma.htm#jt

#

series_ids = {

"Tech Job Openings": "JTS540099000000000JOL", # Professional and business services (often used as a proxy for tech)

"Manufacturing Job Openings": "JTS300000000000000JOL",

"Retail Job Openings": "JTS440000000000000JOL",

# "Food Services Job Openings": "JTS720000000000000JOL",

# https://data.bls.gov/timeseries/LNU04032215

#

# 04 = rate, 03 = level (numbers)

#

"Tech Unemployment": "LNU03032239", # Unemployment for professional and technical services

"Manufacturing Unemployment": "LNU03032232",

"Retail Unemployment": "LNU03032235"

# "Food Services Unemployment": "LNS14000032"

}

# Define the endpoint and parameters for the API request

endpoint = "https://api.bls.gov/publicAPI/v2/timeseries/data/"

headers = {

"Content-Type": "application/json"

}

# Request data for each series

data = {

"seriesid": list(series_ids.values()),

"startyear": "2004",

"endyear": "2024",

"registrationkey": api_key

}

response = requests.post(endpoint, json=data, headers=headers)

json_data = response.json()

# Extract data and create DataFrames for each sector

sector_data = {}

for series in json_data['Results']['series']:

series_id = series['seriesID']

series_name = [key for key, value in series_ids.items() if value == series_id][0]

data_points = [(item['year'], item['value']) for item in series['data']]

df = pd.DataFrame(data_points, columns=['Year', series_name])

df[series_name] = df[series_name].astype(float)

sector_data[series_name] = df.set_index('Year')# Merge job openings and unemployment data for each sector

sectors = ["Tech", "Manufacturing", "Retail"]

df_ratios = pd.DataFrame()

for sector in sectors:

job_openings_col = f"{sector} Job Openings"

unemployment_col = f"{sector} Unemployment"

df_merged = pd.merge(sector_data[job_openings_col], sector_data[unemployment_col], left_index=True, right_index=True)

df_merged[f"{sector} Job Openings to Unemployment Ratio"] = df_merged[job_openings_col] / df_merged[unemployment_col]

if df_ratios.empty:

df_ratios = df_merged[[f"{sector} Job Openings to Unemployment Ratio"]]

else:

df_ratios = df_ratios.join(df_merged[[f"{sector} Job Openings to Unemployment Ratio"]], how='outer')df_job_to_unemp_ratios = df_ratios.groupby(df_ratios.index)[["Tech Job Openings to Unemployment Ratio", "Manufacturing Job Openings to Unemployment Ratio", "Retail Job Openings to Unemployment Ratio"]].mean()

df_job_to_unemp_ratios.head()| Tech Job Openings to Unemployment Ratio | Manufacturing Job Openings to Unemployment Ratio | Retail Job Openings to Unemployment Ratio | |

|---|---|---|---|

| Year | |||

| 2004 | 0.780469 | 0.273507 | 0.349046 |

| 2005 | 0.958135 | 0.363483 | 0.430798 |

| 2006 | 1.167889 | 0.479952 | 0.483758 |

| 2007 | 1.263115 | 0.479159 | 0.489625 |

| 2008 | 0.815361 | 0.260251 | 0.345037 |

# Plot the data

plt.figure(figsize=(14, 8))

plt.plot(df_job_to_unemp_ratios.index, df_job_to_unemp_ratios["Tech Job Openings to Unemployment Ratio"], marker='o', label="Tech Job Openings to Unemployment Ratio")

plt.plot(df_job_to_unemp_ratios.index, df_job_to_unemp_ratios["Manufacturing Job Openings to Unemployment Ratio"], marker='o', label="Manufacturing Job Openings to Unemployment Ratio")

plt.plot(df_job_to_unemp_ratios.index, df_job_to_unemp_ratios["Retail Job Openings to Unemployment Ratio"], marker='o', label="Retail Job Openings to Unemployment Ratio")

plt.title('Job Openings to Unemployment Ratio by Sector (2004-2024)')

plt.xlabel('Year')

plt.ylabel('Ratio of Job Openings to Unemployment')

plt.legend()

plt.grid(True)

plt.show()

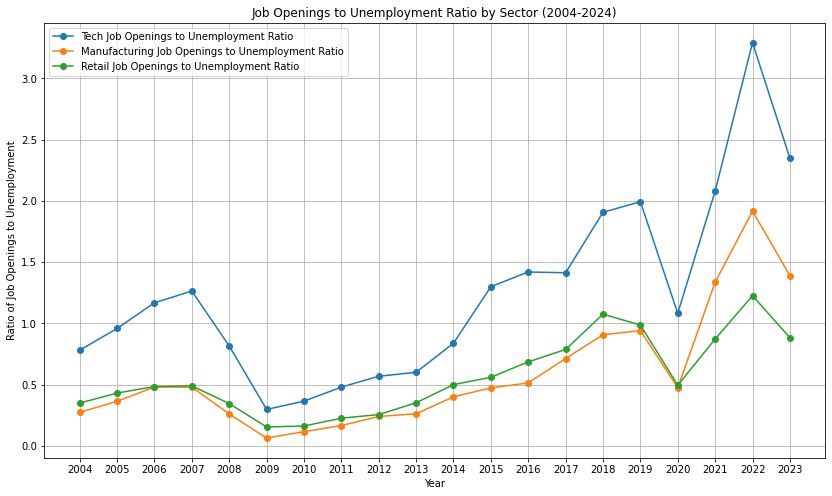

The above chart illustrates the ratio of job openings to unemployment across three sectors: Tech, Manufacturing, and Retail, over the period from 2004 to 2024. The Tech sector consistently shows a higher ratio compared to Manufacturing and Retail, particularly after 2014, where it surpasses a ratio of 1.0, indicating more job openings than unemployed individuals in that sector. The ratio peaks around 2022 at approximately 3.0 before slightly declining in 2023. The Manufacturing sector shows a steady increase in the ratio from around 0.2 in 2009 to about 1.0 in 2022, indicating a tightening labor market. Retail also shows a similar trend, with the ratio increasing from around 0.2 in 2009 to about 1.0 in 2022. However, both Manufacturing and Retail sectors exhibit more fluctuation compared to the Tech sector, particularly noticeable during the 2020-2021 period, reflecting the impact of economic disruptions during that time.

Reflections

Although tech is creating more openings than official unemployment numbers, there are two caveats.

Tech itself changes fast and anyone in tech needs constant re-skilling/up-skilling to cope up with the change.

The definition of “Unemplyment” is tricky. > Unemployment rate The unemployment rate represents the number of unemployed people as a percentage of the labor force (the labor force is the sum of the employed and unemployed). The unemployment rate is calculated as: (Unemployed ÷ Labor Force) x 100.

Not in the labor force: In the Current Population Survey, people are classified as not in the labor force if:

- they were not employed during the survey reference week and

- they had not actively looked for work (or been on temporary layoff) in the last 4 weeks

In other words, people not in the labor force are those who do not meet the criteria to be classified as either employed or unemployed, as defined above. People not in the labor force are asked whether they want a job and if they were available to take a job during the survey reference week. They also are asked about their job search activity in the last 12 months (or since the end of their last job, if they held one in the last 12 months) and their reason for not having looked for work in the most recent 4 weeks.

- they were not employed during the survey reference week and

The value of degrees in fields like business, computer science, and engineering has significantly diminished compared to 30 years ago. While these degrees once paved a reliable path to stable and lucrative careers, today’s landscape is far more competitive, with qualified professionals and offshore workers willing to work for less. As a result, merely obtaining a degree is no longer a guaranteed ticket to success; one must be exceptionally skilled, and this often needs to start before even pursuing the degree. For many, it may be more advantageous to take the risk of business ownership and work for themselves, where they have greater control over their income and career. From the perspective of a seasoned software engineer with over a decade of experience, including leadership roles, the field has become increasingly challenging and less rewarding. If given the chance to start over, they would prioritize gaining experience quickly through startups, learning the intricacies of business, and eventually pursuing entrepreneurship to have more control over their destiny and financial rewards. In essence, a degree alone is not enough anymore; individuals must take proactive control of their careers and explore alternative paths like entrepreneurship to secure their futures.

- Student Debt: Federal Reserve data shows that student debt in the U.S. has skyrocketed, surpassing $1.7 trillion in 2021. This growing debt burden makes it harder for graduates to achieve financial stability, let alone upward mobility.

JOR

The Job Openings Rate (JOR) is defined as the number of job openings on the last business day of the month as a percentage of total employment plus job openings. Mathematically:

$

= ( ) $

Key Components:

- Job Openings: The number of available positions employers are actively recruiting to fill.

- Total Employment: The total number of individuals currently employed in the workforce.

- Denominator: The sum of total employment and job openings represents the total labor market capacity.

Purpose:

- The JOR serves as an indicator of labor demand and provides insights into economic health.

- Higher rates may signal strong demand for workers, while lower rates can indicate reduced hiring activity.

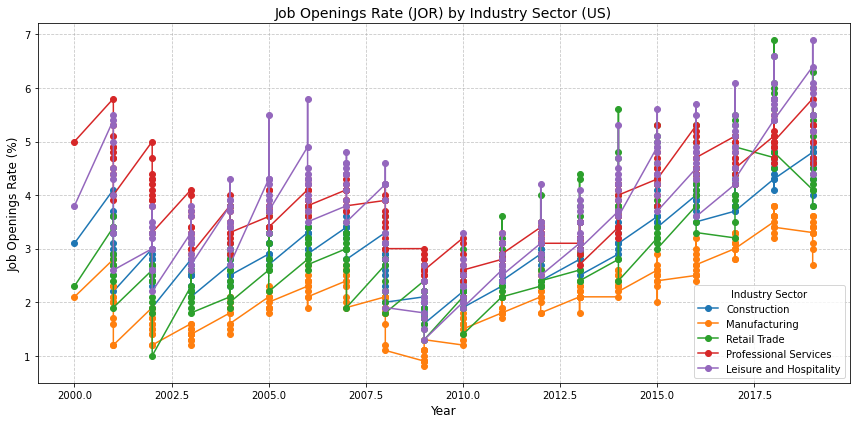

This definition is relevant to the plotted data in your script, where JOR trends are analyzed across various industry sectors.

import requests

import matplotlib.pyplot as plt

import pandas as pd

# Define your BLS API key (replace with your actual API key)

API_KEY = "36aea4409aef4dd787a9ab7107c9d232"

# Define the series IDs for different industries (replace with actual series IDs for JOR)

series_ids = {

"Construction": "JTU000000000000000JOR",

"Manufacturing": "JTU300000000000000JOR",

"Retail Trade": "JTU440000000000000JOR",

"Professional Services": "JTU600000000000000JOR",

"Leisure and Hospitality": "JTU700000000000000JOR",

}

# Define the API URL

BASE_URL = "https://api.bls.gov/publicAPI/v2/timeseries/data/"

# Fetch data from BLS API

def fetch_bls_data(series_id):

payload = {

"seriesid": [series_id],

"startyear": "2000",

"endyear": "2024",

"registrationkey": API_KEY,

}

response = requests.post(BASE_URL, json=payload)

if response.status_code == 200:

data = response.json()

return data["Results"]["series"][0]["data"]

else:

print(f"Error fetching data for {series_id}: {response.status_code}")

return []

# Process the fetched data

def process_data(data):

years = []

values = []

for entry in data:

years.append(int(entry["year"]))

values.append(float(entry["value"]))

return pd.Series(values, index=years)

# Fetch and process data for all series

jor_data = {}

for sector, series_id in series_ids.items():

raw_data = fetch_bls_data(series_id)

jor_data[sector] = process_data(raw_data)

# Combine all data into a single DataFrame

df = pd.DataFrame(jor_data)

# Plot the data

plt.figure(figsize=(12, 6))

for column in df.columns:

plt.plot(df.index, df[column], marker="o", label=column)

# Add chart details

plt.title("Job Openings Rate (JOR) by Industry Sector (US)", fontsize=14)

plt.xlabel("Year", fontsize=12)

plt.ylabel("Job Openings Rate (%)", fontsize=12)

plt.legend(title="Industry Sector", fontsize=10)

plt.grid(True, linestyle="--", alpha=0.7)

# Show the plot

plt.tight_layout()

plt.show()

1b. Social Status and Mobility

Labor Market Saturation and Reduced Returns on Education:

The saturation of the labor market with degree holders has diminished the economic returns of education for many individuals. With more people obtaining degrees, the competition for top-tier jobs has intensified, leading to a situation where a degree alone is no longer sufficient to guarantee upward mobility. This has led to a “credential inflation,” where higher qualifications are needed to stand out, further pushing individuals towards costly graduate education, such as MBAs, which again are becoming increasingly expensive due to M2 inflation.

Strategies to validate:

- Use LinkedIn data scraping for Application-to-job ratio

- % of MBA degrees confered over years (National Center for Education Statistics (NCES) data)

Rise of Elite Education as a Gateway

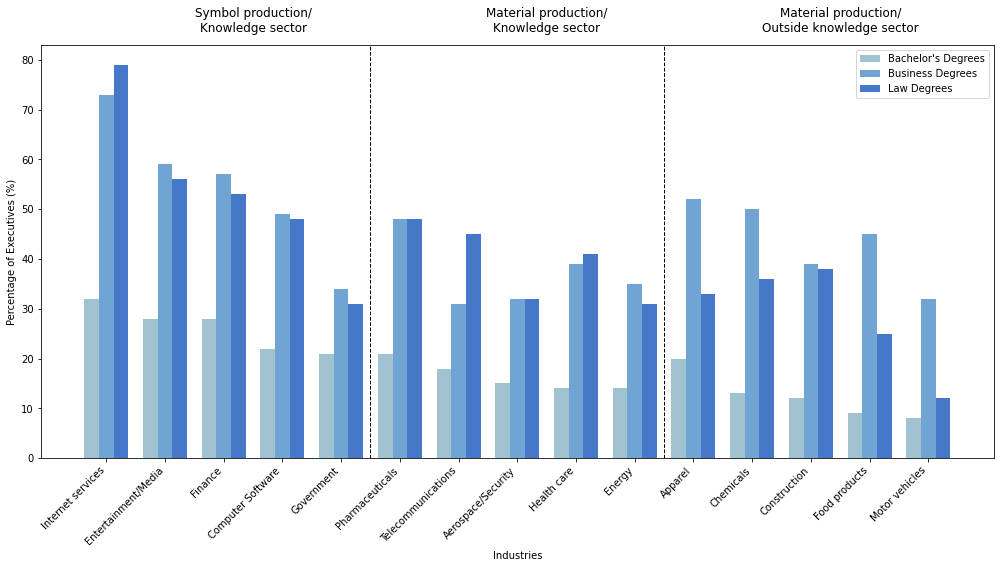

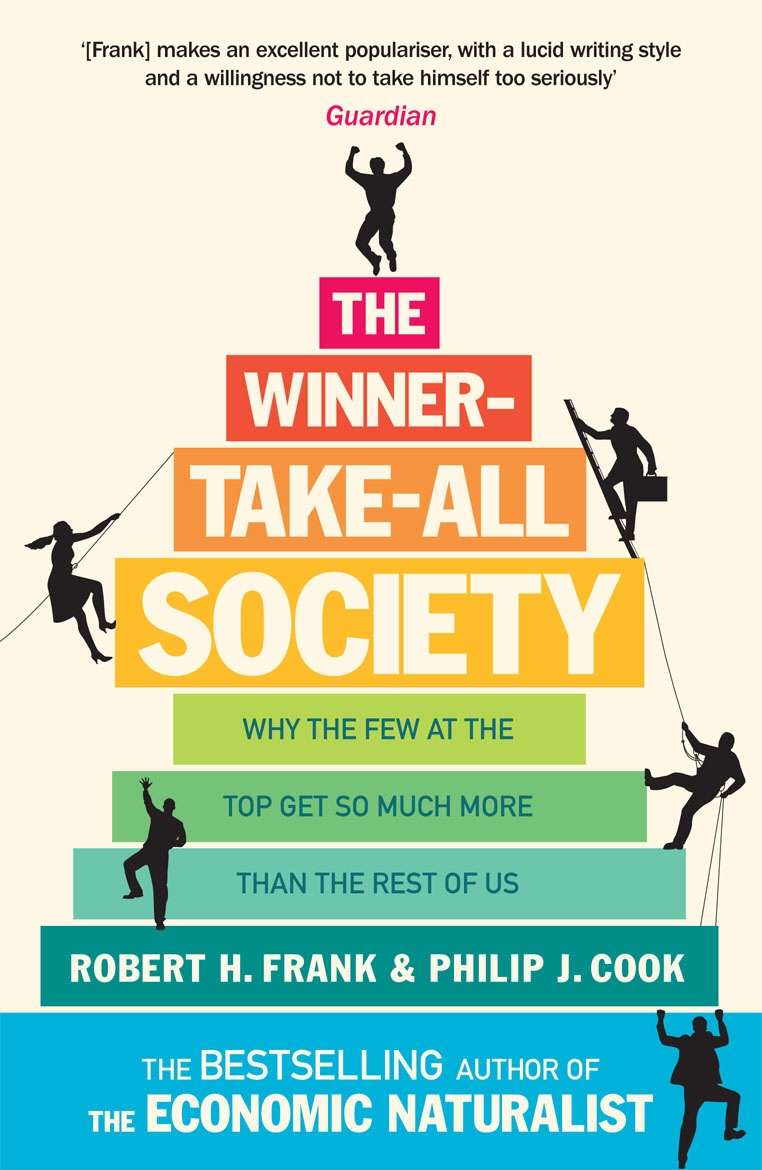

Business Leadership: Frank and Cook discuss how elite business schools (e.g., Harvard Business School, Stanford Graduate School of Business) dominate the pathways to top executive positions in Fortune 500 companies. The networks and brand recognition of these institutions give their graduates a significant edge in the competition for leadership roles.

Legal Profession: The book highlights how top law firms overwhelmingly recruit from a handful of elite law schools (e.g., Harvard, Yale, Stanford). Graduates from these schools have a much higher chance of securing high-paying positions, regardless of their actual performance in law school compared to graduates from less prestigious institutions.

Educational background plays a crucial role in determining career trajectories. Those from elite schools continue to dominate leadership positions, whereas those from non-elite schools find it harder to break into these roles, even if they start at the same level.

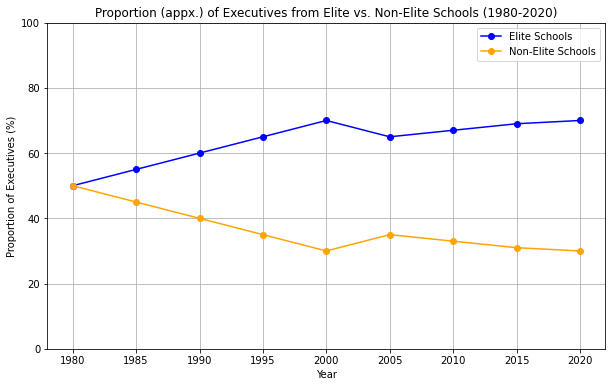

Quantitative Data: The study provides data indicating that over the last few decades, the proportion of executives coming from elite schools has increased, while the proportion from non-elite schools has decreased.

Reference: Frank, R. H., & Cook, P. J. (1995). The Winner-Take-All Society. This book discusses how certain elite institutions have monopolized access to top jobs.

Reference: - Diversity, Hierarchy, and Fit in Legal Careers: Insights from Fifteen Years of Qualitative Interviews https://www.law.georgetown.edu/legal-ethics-journal/wp-content/uploads/sites/24/2019/01/GT-GJLE180004.pdf

Data on Educational Attainment and Professional Success

To create a chart showing the proportion of executives from elite versus non-elite schools from 1980 to 2020, data from various studies indicate the following trends:

1980s: In the early 1980s, around 50% of executives in top U.S. firms had graduated from elite schools, with this figure remaining fairly stable through the decade. Elite schools are often defined as Ivy League institutions and other top-tier universities like Stanford and MIT( Oxford Academic ).

1990s: The 1990s saw a slight increase in the proportion of executives from elite schools, reaching around 55%. This was driven by the increasing value placed on prestigious MBA programs from elite institutions as a key qualification for senior management roles( Oxford Academic ).

2000s: During the 2000s, the proportion of executives from elite schools continued to rise, peaking at around 60-65% by the late 2000s. This trend was supported by the globalization of business and the preference for executives with international educational experiences, often obtained at elite institutions( SpringerLink ).

2010-2020: The proportion of executives from elite schools has stabilized, fluctuating between 60-70%. This period also saw an increase in the importance of non-traditional elite schools, particularly for tech and innovative companies, where elite institutions like Stanford and MIT played a major role( SpringerLink , Oxford Academic ).

Ref - Steven Brint, Sarah R K Yoshikawa, The Educational Backgrounds of American Business and Government Leaders: Inter-Industry Variation in Recruitment from Elite Colleges and Graduate Programs, Social Forces, Volume 96, Issue 2, December 2017, Pages 561–590, https://doi.org/10.1093/sf/sox059 https://academic.oup.com/sf/article-abstract/96/2/561/4622952?login=false - https://link.springer.com/chapter/10.1007/978-3-319-59966-3_5

Educational Backgrounds of American Business and Government Leaders

Steven Brint, Sarah R K Yoshikawa, The Educational Backgrounds of American Business and Government Leaders: Inter-Industry Variation in Recruitment from Elite Colleges and Graduate Programs, Social Forces, Volume 96, Issue 2, December 2017, Pages 561–590, https://doi.org/10.1093/sf/sox059

import matplotlib.pyplot as plt

import numpy as np

# Data from the table

groups = [

"A. Symbol production/Knowledge sector", "A. Symbol production/Knowledge sector",

"A. Symbol production/Knowledge sector", "A. Symbol production/Knowledge sector",

"A. Symbol production/Knowledge sector",

"B. Material production/Knowledge sector", "B. Material production/Knowledge sector",

"B. Material production/Knowledge sector", "B. Material production/Knowledge sector",

"B. Material production/Knowledge sector",

"C. Material production/Outside knowledge sector", "C. Material production/Outside knowledge sector",

"C. Material production/Outside knowledge sector", "C. Material production/Outside knowledge sector",

"C. Material production/Outside knowledge sector"

]

industries = [

"Internet services", "Entertainment/Media", "Finance", "Computer Software", "Government",

"Pharmaceuticals", "Telecommunications", "Aerospace/Security", "Health care", "Energy",

"Apparel", "Chemicals", "Construction", "Food products", "Motor vehicles"

]

# Steven Brint, Sarah R K Yoshikawa, The Educational Backgrounds of American Business and Government Leaders: Inter-Industry Variation in Recruitment from Elite Colleges and Graduate Programs, Social Forces, Volume 96, Issue 2, December 2017, Pages 561–590, https://doi.org/10.1093/sf/sox059 https://academic.oup.com/sf/article-abstract/96/2/561/4622952?login=false

bachelors_degrees = [32, 28, 28, 22, 21, 21, 18, 15, 14, 14, 20, 13, 12, 9, 8]

business_degrees = [73, 59, 57, 49, 34, 48, 31, 32, 39, 35, 52, 50, 39, 45, 32]

law_degrees = [79, 56, 53, 48, 31, 48, 45, 32, 41, 31, 33, 36, 38, 25, 12]

# Define a more soothing color palette

bachelors_color = "#a1c3d1" # Light teal

business_color = "#70a4d3" # Medium teal

law_color = "#4678c9" # Dark teal

# Plotting the trends

x = np.arange(len(industries)) # the label locations

width = 0.25 # the width of the bars

fig, ax = plt.subplots(figsize=(14, 8))

rects1 = ax.bar(x - width, bachelors_degrees, width, label="Bachelor's Degrees", color=bachelors_color)

rects2 = ax.bar(x, business_degrees, width, label='Business Degrees', color=business_color)

rects3 = ax.bar(x + width, law_degrees, width, label='Law Degrees', color=law_color)

# Add vertical lines to visually segregate the industry groups

ax.axvline(x=4.5, color='black', linestyle='--', lw=1) # End of Symbol production/Knowledge sector

ax.axvline(x=9.5, color='black', linestyle='--', lw=1) # End of Material production/Knowledge sector

ax.text(2.5, 85, 'Symbol production/\nKnowledge sector', ha='center', va='bottom', fontsize=12)

ax.text(7.5, 85, 'Material production/\nKnowledge sector', ha='center', va='bottom', fontsize=12)

ax.text(12.5, 85, 'Material production/\nOutside knowledge sector', ha='center', va='bottom', fontsize=12)

# Add some text for labels, title and custom x-axis tick labels, etc.

ax.set_xlabel('Industries')

ax.set_ylabel('Percentage of Executives (%)')

#ax.set_title('Percentage of Executives with Elite Degrees by Industry Group')

ax.set_xticks(x)

ax.set_xticklabels(industries, rotation=45, ha="right")

ax.legend()

fig.tight_layout()

plt.show()

https://x.com/cremieuxrecueil/status/1831463564575699266/photo/1

!

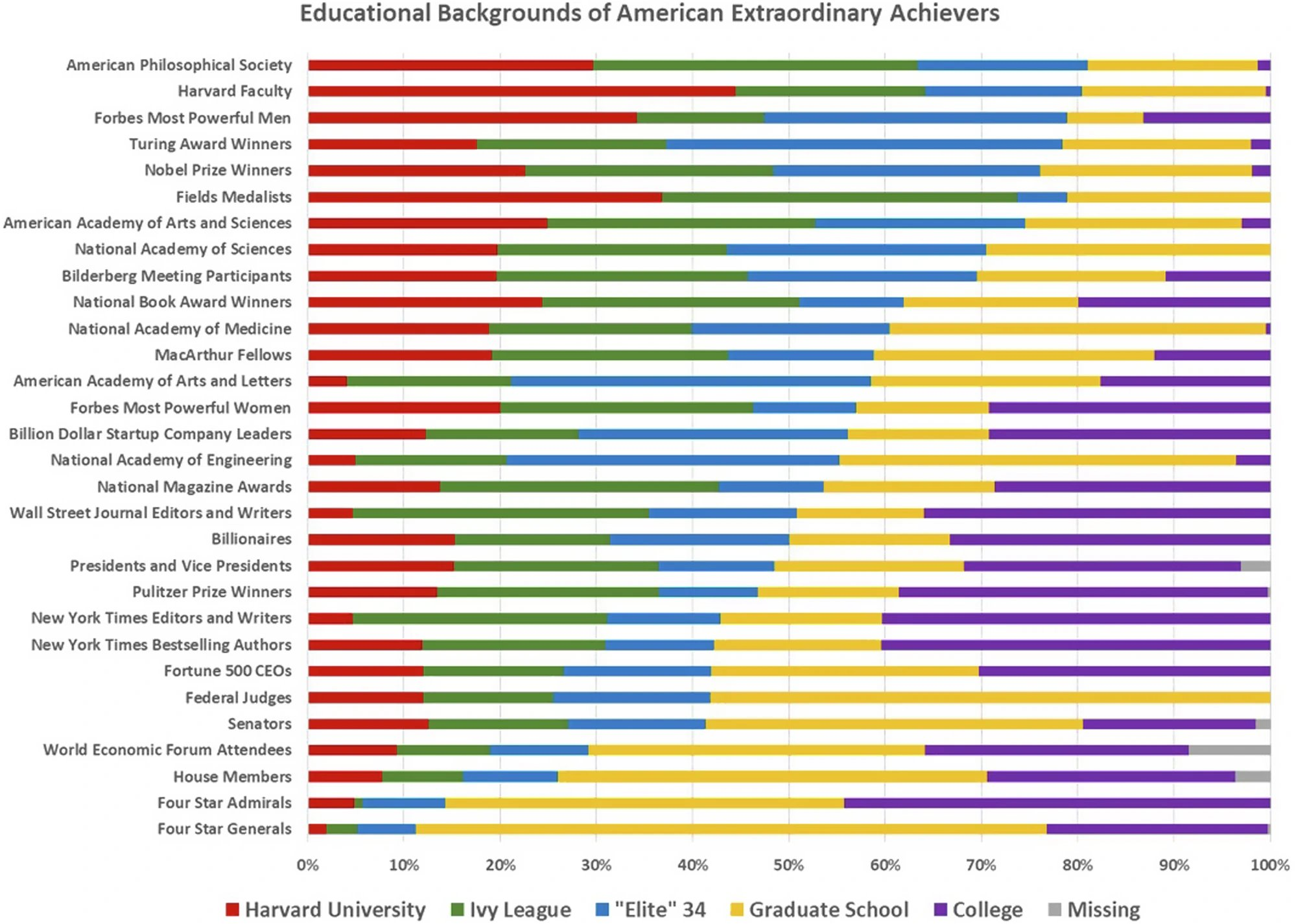

!

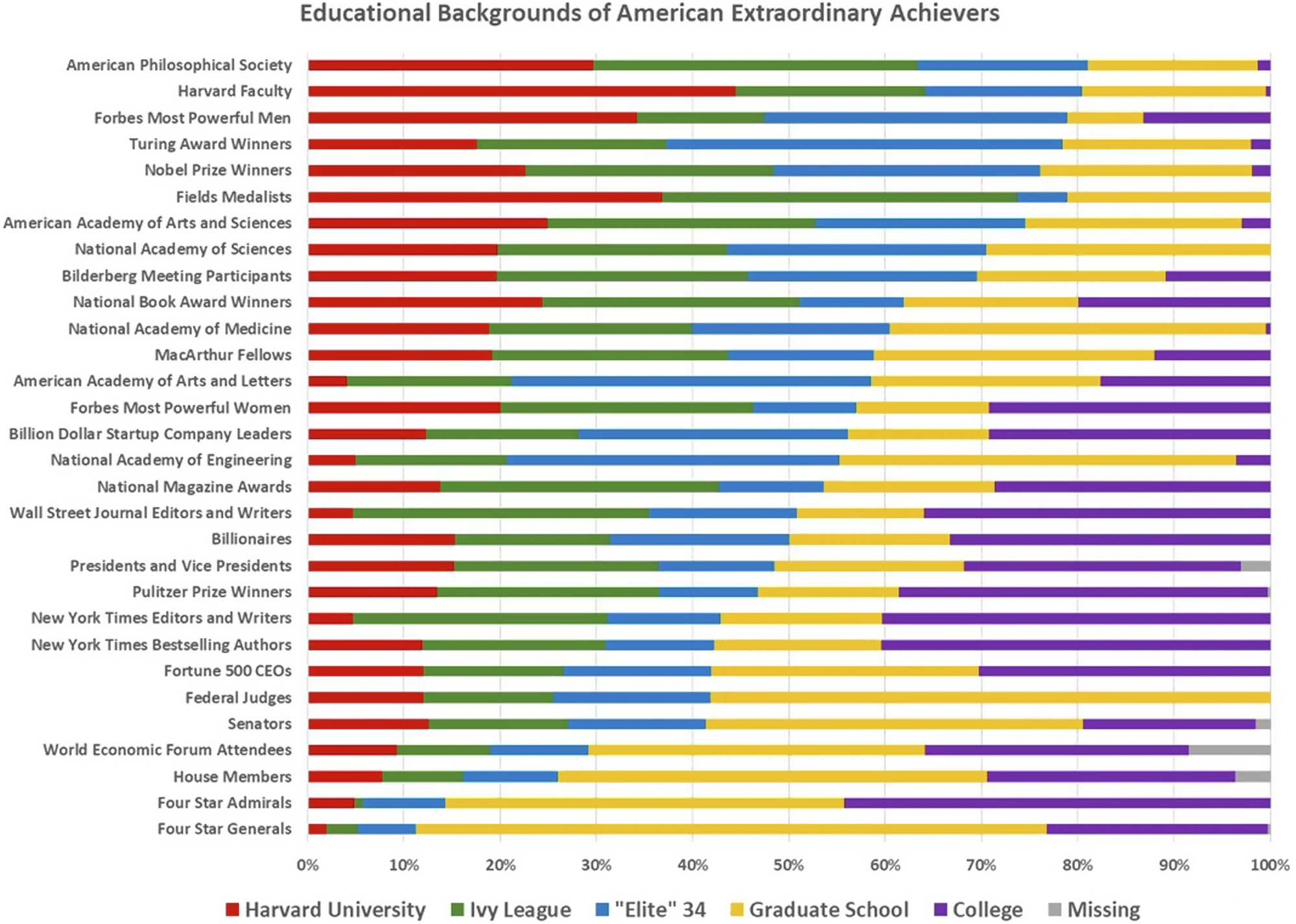

The chart illustrates the educational backgrounds of extraordinary American achievers across various categories. For example, Harvard University alumni account for approximately 50% of American Philosophical Society members and 35% of Forbes’ most powerful men. Graduate School graduates make up the majority in categories like National Academy of Medicine (over 70%) and Nobel Prize winners (about 60%). On the other hand, Ivy League graduates represent significant shares in categories like Pulitzer Prize winners (40%) and Four-Star Generals (20%). Some categories show missing educational information, such as Senators (around 10%).

In the last generation or two, the funnel of opportunity in American society has drastically narrowed, with a greater and greater proportion of our financial, media, business, and political elites being drawn from a relatively small number of our leading universities, together with their professional schools. The rise of a Henry Ford, from farm boy mechanic to world business tycoon, seems virtually impossible today, as even America’s most successful college dropouts such as Bill Gates and Mark Zuckerberg often turn out to be extremely well-connected former Harvard students. Indeed, the early success of Facebook was largely due to the powerful imprimatur it enjoyed from its exclusive availability first only at Harvard and later restricted to just the Ivy League

Let’s explore what are demographical and academic attributes of groups attaining eite education

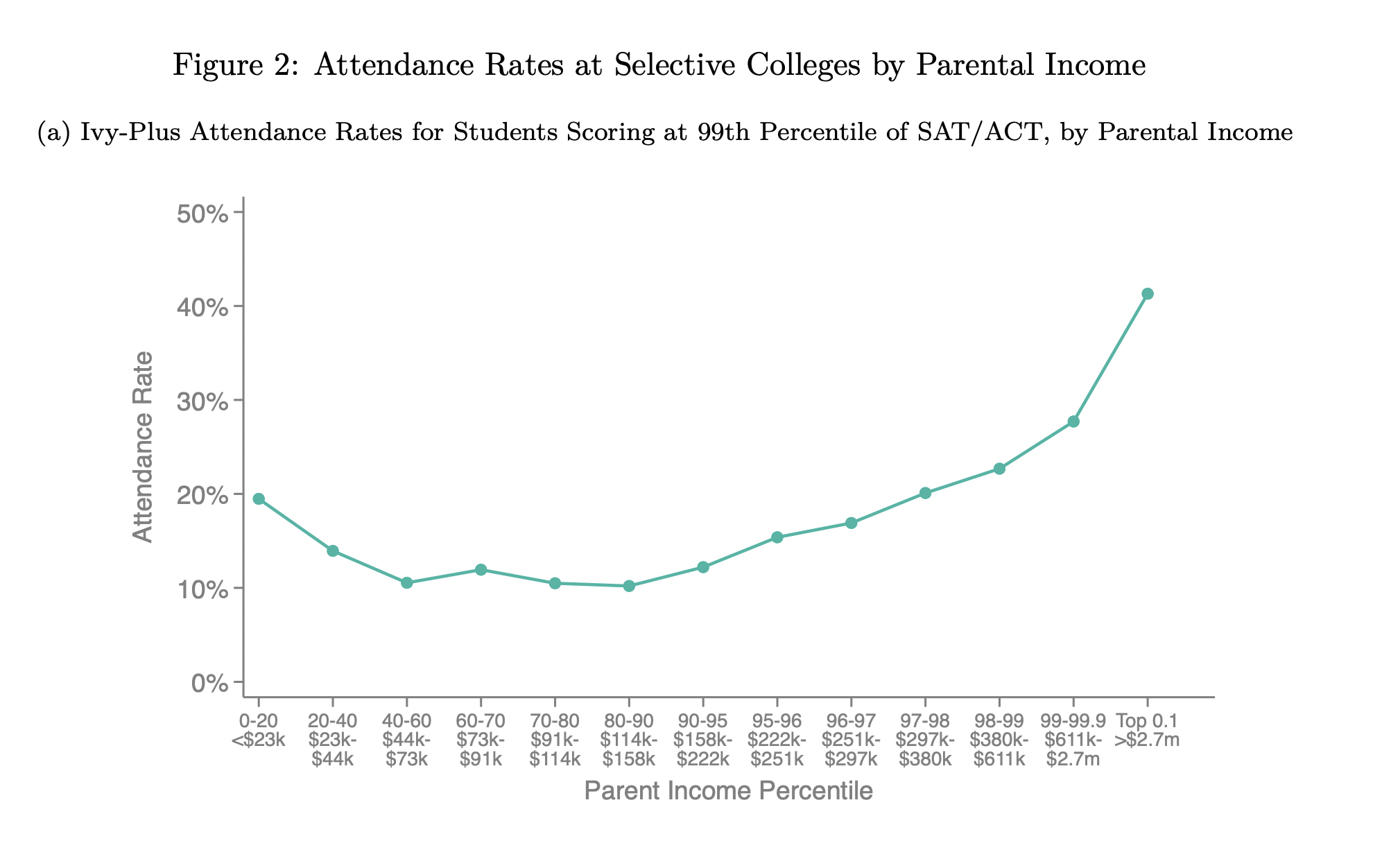

Children from families in the top 1% are more than twice as likely to attend an Ivy-Plus college (Ivy League, Stanford, MIT, Duke, and Chicago) as those from middle-class families with comparable SAT/ACT scores. Two-thirds of this gap is due to higher admissions rates for students with comparable test scores from high-income families

The highincome admissions advantage at private colleges is driven by three factors: - (1) preferences for children of alumni (legacies) - (2) weight placed on non-academic credentials, which tend to be stronger for students applying from private high schools (feeder) that have affluent student bodies, - (3) recruitment of athletes, who tend to come from higher-income families.

References

- Chetty, R., Deming, D., & Friedman, J. (2023). Diversifying Society’s Leaders? The Determinants and Causal Effects of Admission to Highly Selective Private Colleges. National Bureau of Economic Research. https://doi.org/10.3386/w31492

Development cases, where donations influence admissions, are common among Ivy Plus schools. For example, Jared Kushner’s father donated $2.5 million to Harvard before his son’s acceptance. Schools like USC also heavily weigh such cases. Political and celebrity connections—like children of U.S. Senators or famous actors—often sway admissions. This practice highlights how wealth and influence can shape access to top-tier education.

The push for legacy admissions persists, even as it faces criticism. Legacy students, those with family ties to alumni, receive special consideration, despite calls to end the practice. Ivy League schools, and some state flagships like Michigan and UVA, continue to favor legacies. For instance, Johns Hopkins recently ended legacy admissions, aiming for more socio-economic diversity, but this may impact future alumni donations.

Athletics also play a crucial role in admissions at elite schools. Ivies admit a notable number of student-athletes (up to 10% of their student bodies). Brown, with 910 athletes, parallels Michigan despite a smaller overall student body. Schools like Stanford and Duke also recruit heavily for sports like sailing and lacrosse, reinforcing the socioeconomic skew in admissions, with wealthier, predominantly white students disproportionately represented.

Unfair Advantage

Many universities offer tuition remission to employees’ children, with some covering up to 100% of tuition if the student attends the parent’s institution, but only 50-75% if they attend another school. This incentivizes universities to admit employees’ children, minimizing financial loss. Employees’ families, particularly those in academic households, often have greater cultural and academic capital, giving them an admissions advantage. Children of professors or staff, exposed to academic environments and cultural resources, may appear more competitive than wealthier, first-generation applicants, who lack such insider knowledge.

# Data for plotting

years = list(range(1980, 2021, 5))

elite_schools = [50, 55, 60, 65, 70, 65, 67, 69, 70]

non_elite_schools = [100 - x for x in elite_schools]

# Plotting the data

plt.figure(figsize=(10, 6))

plt.plot(years, elite_schools, marker='o', linestyle='-', color='blue', label='Elite Schools')

plt.plot(years, non_elite_schools, marker='o', linestyle='-', color='orange', label='Non-Elite Schools')

# Adding titles and labels

plt.title('Proportion (appx.) of Executives from Elite vs. Non-Elite Schools (1980-2020)')

plt.xlabel('Year')

plt.ylabel('Proportion of Executives (%)')

plt.ylim(0, 100)

plt.xticks(years)

plt.grid(True)

# Adding a legend

plt.legend()

# Show plot

plt.show()

The Winner-Take-All Society

How certain elite institutions have monopolized access to top jobs.

Frank, R. H., & Cook, P. J. (1995). The Winner-Take-All Society

Concentration of Rewards in Elite Institutions: Argument: Frank and Cook argue that in many fields, the rewards (jobs, salaries, opportunities) are increasingly concentrated among those who graduate from elite institutions. These institutions, such as Ivy League universities in the U.S., have become gatekeepers to the most lucrative and prestigious careers. Example: The authors discuss how a small number of elite schools produce a disproportionately high number of individuals in top positions across various industries, from law and finance to academia and government.

https://academic.oup.com/qje/article/137/2/845/6449025

Winner-Take-All Markets: Concept: The book introduces the concept of “winner-take-all markets,” where small differences in talent or credentials can lead to vastly different outcomes in terms of success and earnings. In these markets, those at the very top capture the majority of rewards, while the rest receive significantly less. Data: The book cites examples such as the concentration of top lawyers from a handful of law schools or CEOs who predominantly come from elite business schools. This concentration means that individuals from non-elite institutions find it increasingly difficult to compete for top-tier positions.

Impact on Social Mobility: Argument: The monopolization of access to top jobs by elite institutions exacerbates inequality and reduces social mobility. As these institutions become more selective and expensive, only individuals from affluent backgrounds can afford the education and connections needed to access these opportunities. Data: The book discusses how the children of affluent families are more likely to attend elite institutions, perpetuating a cycle of privilege. In contrast, those from less privileged backgrounds face significant barriers to entry, even if they have similar levels of talent or ambition.

Pedigree: How Elite Students Get Elite Jobs” by Lauren A. Rivera